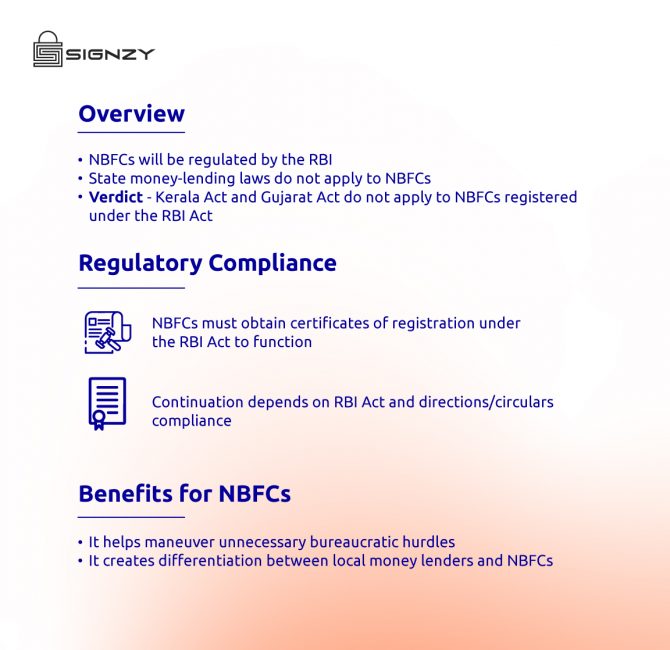

Last week, the Supreme Court held that Non-Banking Financial Companies (NBFCs) regulated by the Reserve Bank of India could not be regulated by individual state enactments.

A bench of Justices Ramasubramanian V and Hemant Gupta said NBFCs play a vital role in contributing to the country’s financial health, whose operations are controlled by RBI. Therefore, it said that the Reserve Bank of India has no say in such a relevant matter of vital interest. It would strike at the fundamentals of the statutory control vested in the Reserve Bank of India.

“It may be true that many times RBI may not be controlling the rate of interest charged by NBFCs on the loans advanced by them. It does not mean that they have no power to step in,” the bench said.

The Supreme Court examined whether Non-Banking Financial Companies regulated by the Reserve Bank of India could also be regulated by specific State enactments such as the Kerala Money Lenders Act, 1958 and the Gujarat Money Lenders Act, 2011.

The fact that the Chapter IIIB of the RBI Act assigns a supervisory role for the Reserve Bank of India to oversee and regulate the NBFCs’ functioning, including all their activities, automatically comes under the scanner of the RBI. This applies to the NBFCs from their inception (registration) till the time of their commercial denouement (winding up/cancellation).

“As a consequence, the single aspect of taking care of the interest of the borrowers which is sought to be achieved by the State enactments gets subsumed in the provisions of Chapter IIIB,” the bench said.

The Supreme court also said it believed that the Kerala Act and the Gujarat Act would not apply to all NBFCs registered under the RBI Act, which the RBI regulates.

Therefore, the bench stated that all the appeals the NBFCs filed against the Kerala High Court’s judgment are standing and allowed. Similarly, the appeals the State of Gujarat filed against the judgment of the Gujarat High Court are wholly dismissed.

What It Means

The statement by the Supreme Court comes as a massive breath of fresh air for NBFC in particular and the fintech industry as a whole. None of the RBI-regulated financial companies need to get tangled in multiple jurisdictions and unnecessary compliance complications. Contradictions between jurisprudence are also apparent and transparent.

Even then, financial companies still need to follow many regulatory compliances. For this, they need reliable fintech service providers to ensure good service. Signzy can get you the apt products and services you seek. With our customizable AI-driven API resources for KYC, Onboarding, etc., which are absolutely regulations compliant, you can make all your financial technology processes optimized to the best degree.

Key Takeaways

- The Reserve Bank of India(RBI) will unequivocally regulate Non-banking financial companies (NBFCs), and state money-lending laws will have no applicability to them.

- The verdict was that the Kerala Act and the Gujarat Act would have no application to the NBFCs registered under the RBI Act and regulated by the RBI.

- No NBFC can begin or carry on business without obtaining a registration certificate under the RBI Act; their continuation in business would depend upon compliance with the RBI Act and circulars/directions issued by the RBI.

- This is impactful news for NBFCs as this will help maneuver unnecessary bureaucratic hurdles.

- It creates a strict differentiation between local money lenders and Non-Banking Financial Companies.

About Signzy

Signzy is a market-leading platform that is redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering totally customizable workflows. It gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru, and it has a strong presence in Mumbai, New York, and Dubai.

Visit www.signzy.com for more information about us.

You can reach out to our team at reachout@signzy.com

Written By:

Signzy

Written by an insightful Signzian intent on learning and sharing knowledge.